|

| Photo by Karolina Grabowska |

In October 2023, the United States saw a decline in the annual inflation rate, dropping to 3.2% compared to 3.7% in both September and August. This figure also fell below the market predictions of 3.3%.

Here's a breakdown of the data:

- Energy costs experienced a significant decrease of 4.5%, compared to the slight decline of -0.5% in September. Gasoline prices dropped by 5.3%, utility (piped) gas service fell by 15.8%, and fuel oil saw a substantial decline of 21.4%.

- Prices for food increased at a more moderate pace of 3.3%, down from 3.7% in the previous month. Similarly, shelter costs rose by 6.7% (compared to 7.2%), and new vehicles saw a slower increase at 1.9% (versus 2.5%). Conversely, prices for used cars and trucks continued to decline, registering a -7.1% change.

- On the other hand, prices rose at an accelerated rate for apparel, increasing by 2.6% compared to 2.3% in the prior month. Medical care commodities experienced a higher inflation rate of 4.7%, up from 4.2%, and transportation services saw a marginal increase from 9.1% to 9.2%.

According to the press release from the Bureau of Labor Statistics (BLS), the index for shelter continued its upward trend in October, compensating for a decrease in the gasoline index and resulting in a seasonally adjusted index that remained stable throughout the month. The energy index, on the other hand, saw a 2.5% decrease, attributed to a notable 5.0% decline in the gasoline index, which more than offset increases in other energy component indexes.

So what does this mean for the financial markets?

The prevailing sentiment among most economists is that the FED has concluded its hiking cycle.

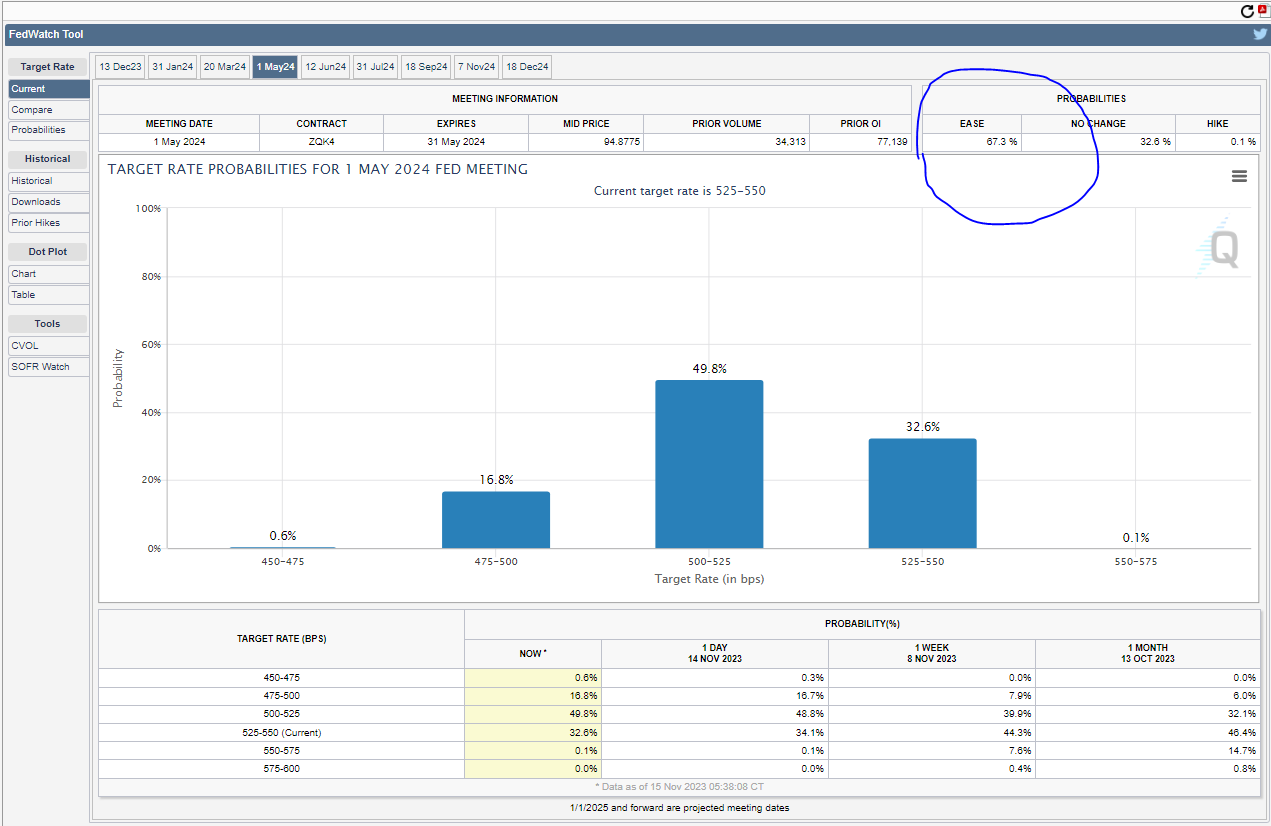

Powell asserted last week that if the need arises for additional policy tightening, they will not hesitate to take appropriate measures. Interestingly, financial markets are presently foreseeing a potential rate hold in December meeting and a reduction/cut in May, as indicated by CME Group's FedWatch tool.

Some economists have expressed the view that the trajectory of the economy avoiding a recession is uncertain. Nevertheless, there is an anticipation of a sustained rally in the stock market as people are accepting the likelihood of higher interest rates has diminished. This perception is expected to contribute to upward movements in both stock and bond prices, consequently driving down bond yields.

While recent positive indicators may suggest a favorable trend, certain economists offer a cautious perspective, emphasizing that inflation has a considerable distance to cover before aligning with the Federal Reserve's 2% target. Additionally, they highlight a rise in consumers' inflation expectations during October.

Will Compernolle, a macro strategist at FHN Financial in New York, expressed reservation, stating, "Declines in energy, core goods prices, and a slowdown in shelter inflation, which were the primary factors behind October's disinflation, are merely the outer layers of the Federal Reserve's 'inflation onion.' These factors are not expected to sustain disinflation indefinitely, making it premature to declare the end of the battle against inflation."

{kind=link}

0 Comments